In our beginning of the year outlook for 2022 we had pure conviction that US consumer price levels would remain elevated with reduced acceleration (relative to 2021), and the supply chain crisis would assume to ease thought this year. Plainly, we still stand on our conviction. We did estimate that we would see tightening labor conditions within the US economy though July’s jobs report showed that the labor conditions in the US are “robust”. These dynamics are more important than ever for the near-future of the US economy as following the second consecutive 75bps hike from the FOMC in July, we were left with a notice from Jerome Powell that the Fed will essentially drop forward guidance and become “data dependent” going forward.

Data dependency ?

Data dependency from the Fed as a substitution for forward guidance can be highly nebulous to all, but we should revisit the econ-101 days to unpack this picture. Despite the complexities of the Federal Reserve’s framework, we must remember that the Fed is tied to its dual-mandate of maximum employment and price stability (in no particular order of course). This should imply that the Fed is closely monitoring inflation and labor statistics to guide them on their impending policy decisions.

Dive into the Data

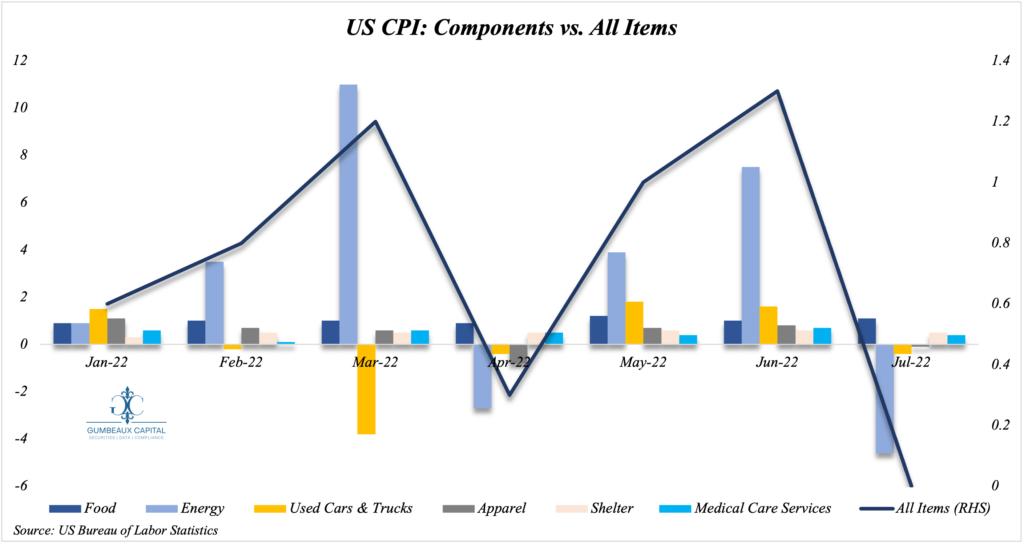

It is highly evident that the Fed has been using its tool-kit to fight inflationary pressures as we saw a 0.3% M/M Core CPI print in July. This is a substantial landmark for a data dependency framework as a 1.4% drop in CPI from June marks as the largest M/M decline since the 1980s. Moreover on the inflation picture, the NFIB relayed that for small market enterprises (SMEs) a net 37% of SMEs plan price hikes, which is down 12 points from June. This is highly indicative of an inflection point in US inflation momentum, but we must keep in consideration the composition of decelerating inflation to grasp a clear macro-picture (see Figure 1).

We can note that the culprits of the M/M move down in CPI is the more cyclical components such as energy (light blue), and used cars & trucks (gold). From a high level point of view, the supply chains on these components have not improved substantially from their tightest conditions, so the evidence of demand destruction is starting to build. Another dynamic to keep an eye on is the relative stickiness of inflation within components such as food and shelter, in which is further indication of the waning of the “soft-landing” narrative for the US Economy.

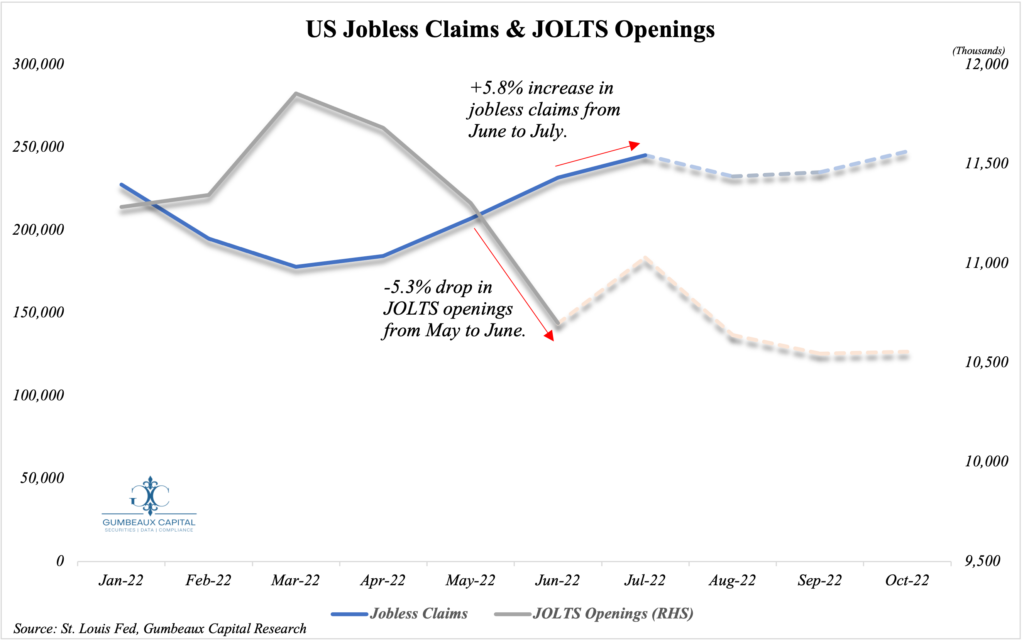

When we look at labor market dynamics, we have a similar picture to inflation; where we have labor market conditions peaking as well (see Figure 2).

Despite July’s NFP data coming in hot, jobless claims and JOLTS data provides a sobering picture.

While we saw a red hot NFP data print for the month of July, the jobless claims count has been rising as we see increased levels of layoffs (highly-evident in tech) as cost of capital continues to rise for firms. JOLTS data paints the same picture as we have seen a consistent drop in job openings since February. We project that jobless claims will initially fall in July due to the relatively improved business conditions seen in July, allowing for more job openings, but the picture will continue to extrapolate the macro environment with slightly lower job openings and increased jobless claims; especially as the labor-force-participation-rate remains below pre-pandemic levels.

Nonetheless, with promising inflation trends, but sobering underlying data with labor markets, the Fed has its work cut out for them. Going forward on a data dependency framework in this particular macro-environment practically forces the Fed to now chose whether to (mainly) focus on reducing price pressures, or to maintain employment levels. The question going forward is; which does the Fed see as the largest threat to the economy? Judging from the recent talking points from this year’s FOMC meetings, one can move with conviction that the Fed will continue to focus on fighting inflation unequivocally.

Bracing for a rough landing

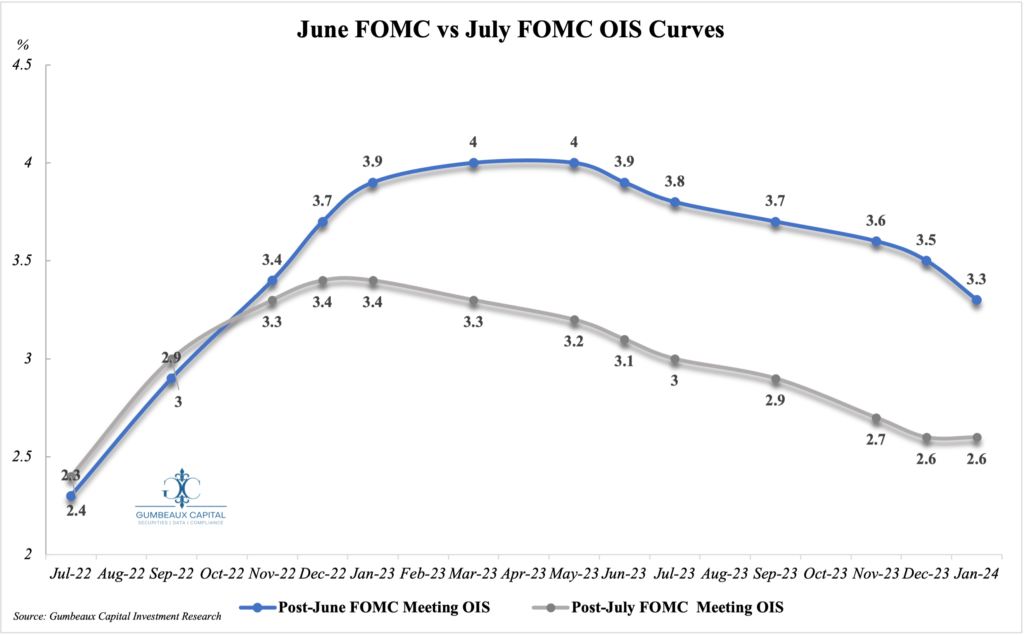

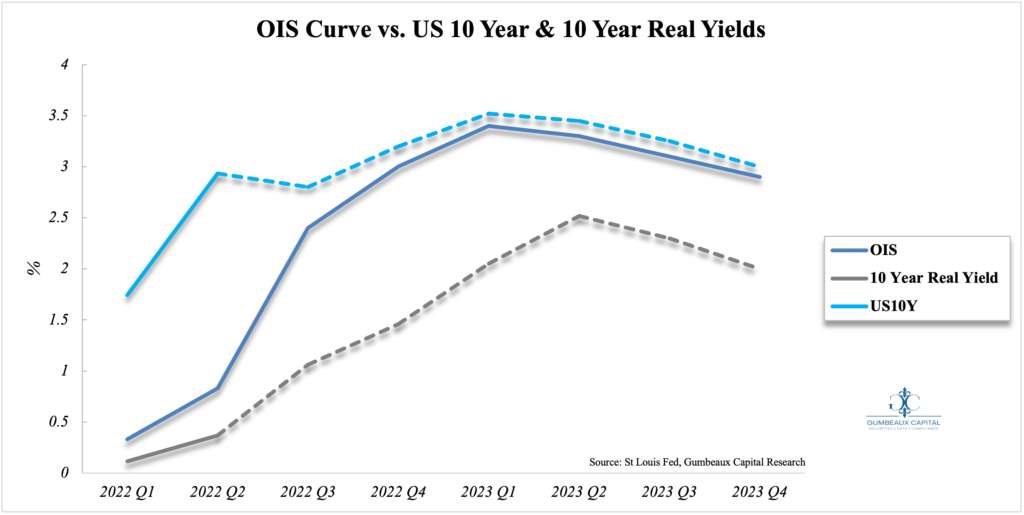

Assuming that we will continue our inflation data trajectory, and continue to get a price-stability-oriented Fed, we can extrapolate that we may see a case to where the Fed may not have to be as aggressive versus the picture we saw in June (see Figure 3).

The OIS Curve is pricing in 3 fewer hikes in 2023 following July’s FOMC meeting.

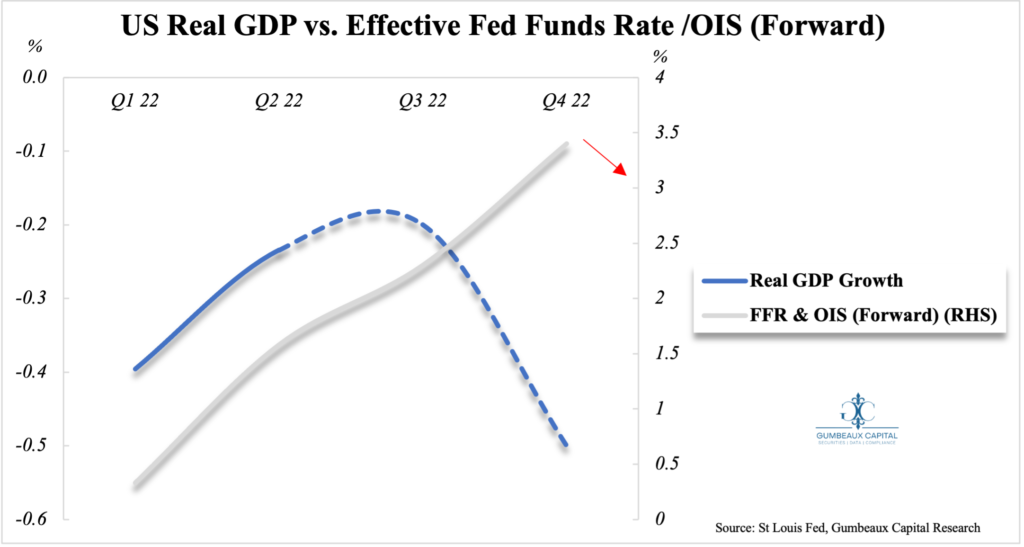

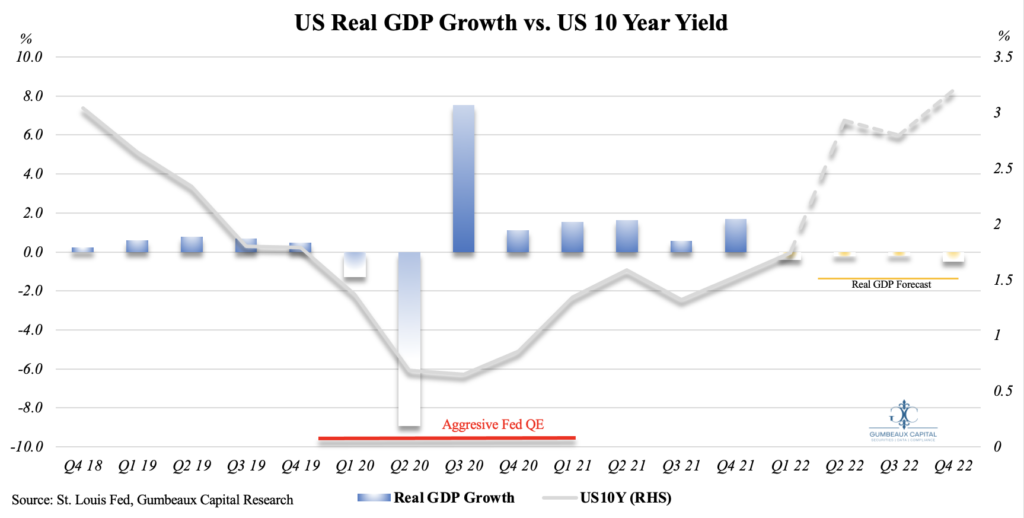

We must keep in mind that a scenario where the Fed prevails victorious in its fight against inflation may not be the sole catalyst to a less aggressive (forward-looking) Fed. The Fed may have to become more accommodative to the economy as the prospects for a “rougher than expected landing” continue to grow (see Figure 4, 5, & 6).

We have forecasted Real GDP Growth to slow substantially into further negative territory (-0.5%) over the remainder of 2022 based on our readings of the labor market, the 2s/10s curve, and the FFR/10s curve.

These forecasted dynamics have presented prospects of a rise, and then subsequent fall in 10 year nominal and real yields over the next 16 months as per our forecast.

When putting our growth forecasts into context with 10 year yields, we can exogenously extrapolate that we could expect real GDP growth to resume in H1 2023.

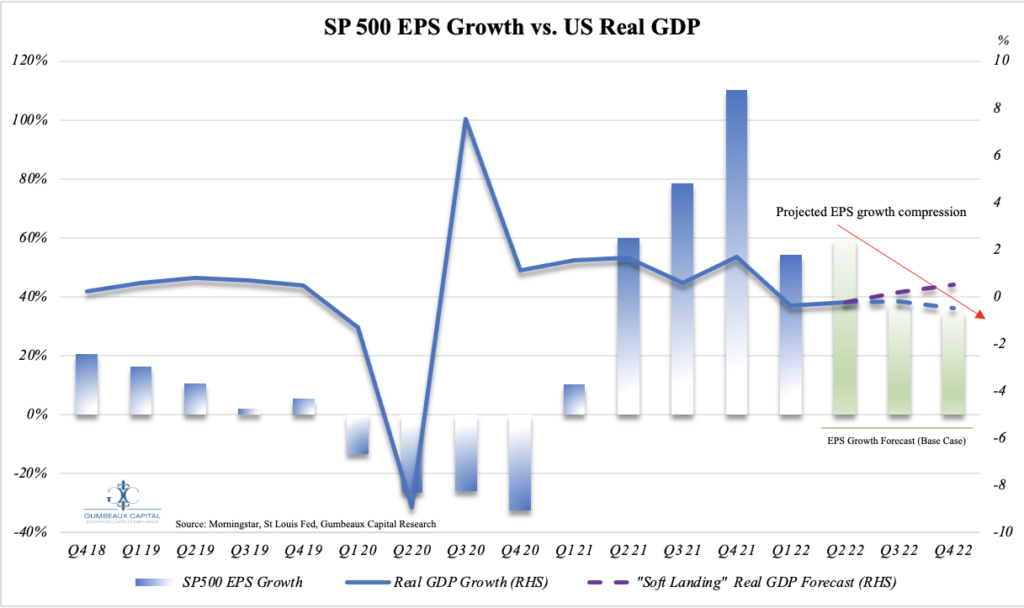

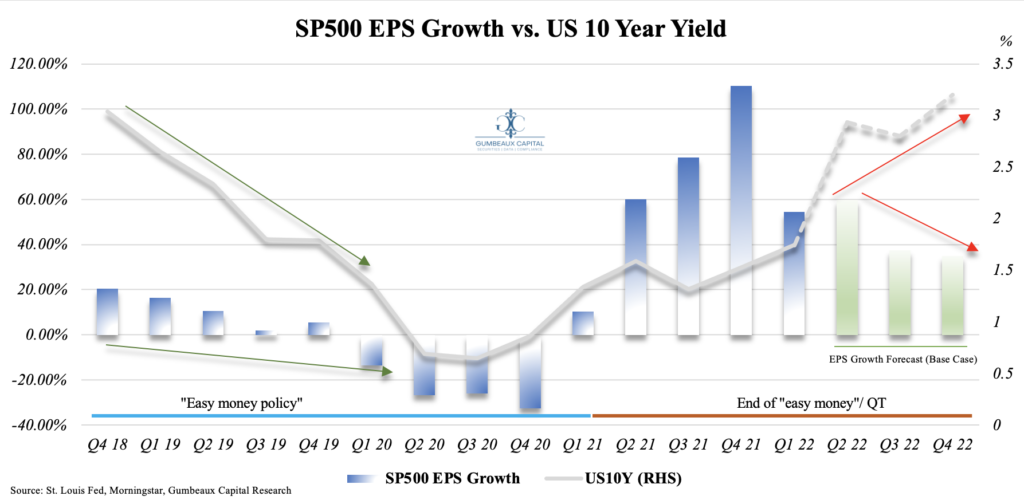

The given data has given a compelling feel for fixed income going forward vs equities. Though Q2 earnings has been relatively upbeat, which is a certain catalyst for the recent market rally, we do not expect EPS growth to continue strengthening from a broad basis; even in a goldilocks “soft landing” scenario (see Figure 7).

We forecast a 41.44% compression in S&P 500 EPS growth through the end of the 2022 (9.2% annual growth rate) regardless of growth scenarios.

As the Fed continues to reduce its balance sheet, expect to see divergence from previous trends of lower yields amidst economic uncertainty. This is indicative that investors should utilize bonds as a risk ballast, and a supplementary yield enhancer in their portfolios in the event we begin to see consistent reduction in inflation (see Figure 8).

The given environment provides us with conviction that bonds will unchain themselves from relatively high correlations with equity performance going into H1 2023.

Rough landing playbook

Our forecasts are not to say that equities have an outright pessimistic outlook going into the latter half of H2 2022 and H1 2023, as we saw very few proponents for equities going into H12022. Yes, financial conditions are getting tighter amidst a broad based rise in cost of capital and slight demand destruction, but it is key to note that the US is still in a position to outperform the rest of the world in terms of earnings growth. This will certainly maintain ample levels of inflows into US capital markets. Equities are positioned to simply take another “breather”, although high quality (healthy margins, high operating leverage, and warrantable valuations etc. ) equities can see excess yield within this environment. All-in-all a move higher in the capital structure and a tactical tilt towards government bonds (2s/10s flatteners) may provide great risk-adjusted opportunities for investors.