The 1st quarter of 2022 have presented us with some interesting dynamics that will ultimately change the global economic outlook for all going forward. Many of the dynamics have lied under the umbrella of geopolitical tensions, economic (incl. energy) policy shifts and “normalizations”. We will uncover and contextualize the complex dynamics and present you with potential macro headwinds and tailwinds forged by the ongoing developments.

Russia-Ukraine Conflict

Serving as the “elephant in the room” the Russia-Ukraine conflict has served as the main source of volatility in 1Q2022. In October of 2021, many reports transpired that contingents of Russian troops and military hardware were being moved to the Russian-Ukrainian border. These reports came in tandem with reports that Russia had already inhibited access to 2/3rds of the Azov sea which borders the Russian-annexed Crimean Peninsula to the north. Now, as of 02/22/2022, Vladimir Putin has executed a decree that recognizes the separatist regions of Ukraine (Donetsk and Luhansk) following a Russian Security Council meeting held on 02/21/2022 [See figure 1].

These events were shortly followed by a statement made by Ursula von der Leyen, “The recognition of the two separatist territories in Ukraine is a blatant violation of international law, the territorial integrity of Ukraine and the Minsk agreements. The EU and its partners will react with unity, firmness and with determination in solidarity with Ukraine.” This comment from the President of the EU Commission accentuates the EU’s disposition on the Russian initiatives which is ultimately based on the geopolitical position of NATO.

Pre Invasion

With concerns from NATO, many expect there to be sanctions formulated against Russia contingent on an “unlawful” encroachment of the Ukrainian territories. This disposition can also be seen as US Secretary of State Anthony Blinken expressed, “We’ve been clear if any Russian military forces move across Ukraine’s border, that’s a renewed invasion. It will be met with swift, severe and a united response from the United States and our partners and allies.” It is also key to contextualize the developments from the UN security council meeting held on 02/21/2022. The UNSC meeting carried some mixed assessments as various nations made many statements agin to the Russian initiatives such as: US Ambassador and Permanent Representative to the UN, Linda-Thomas Greenfield expressing, ” This is nonsense, we know what they really are.” Greenfield even went to the lengths of accusing Russia of creating “a pretext of war.” Kenyan Ambassador and Permanent Representative to the UN, Martin Kimani stated, “It has been assaulted, as it has been by other powerful states in the recent past. We call on all member states to stand behind the Secretary-General in asking him to rally us to the standard of defending multilateralism. We also call on him [Putin] to bring his [Putin] good offices to bear to help the concerned parties resolve the situation by peaceful means.” These invasion-adverse statements were mostly made akin by (mostly western) other nations. These statements were then variegated by the likes of China and India as China’s Permanent Representative to the UN Zhang Jun, expressed, “[global delegates] should continue dialogue and consultation and seek reasonable solutions,” and “All parties concerned must exercise restraint, and avoid any action that may fuel tensions,” and to “welcome and encourage every effort for a diplomatic solution.” India’s Permanent Representative to the UN, T.S. Tirumurti expressed a similar sentiment to China’s Zhang Jun as he stated, “[RU-UKR conflict] can only be resolved through diplomatic dialogue”, and said: “We need to give space to the recent initiatives undertaken by parties which seek to diffuse tensions.”

Russian Sanction Playbook (Pre Invasion)

While the proposition of further sanctions against Russia are certainly evident due to the now onset (and growing) invasion of Ukraine, it is key to contextualize the pre-invasion sanctions imposed on Russia to understand the perpetual dynamics of what the post-invasion sanctions will be.

EU Sanctions (Pre Invasion)

Sanctions from the EU remained relatively light following Putin’s decision to recognize Ukraine’s separatist territories. Sanctions were imposed on all members of the lower house of the Russian parliament who voted in favor of the recognition of the breakaway regions, freezing any assets they have in the EU and banning them from traveling to the EU. EU sanctions also included import bans on goods from the non-government controlled areas of the Donetsk and Luhansk oblasts; prohibition to finance the Russian Federation, its government and Central Bank via restraining the ability of the Russian state and government to access the EU’s capital and financial markets and services were also a component of EU sanctions.

US Sanctions (Pre Invasion)

Joe Biden’s “first tranche” of sanctions included sanctions on two of Russia’s state-owned banks – VEB and Promsvyazbank – and blocked Russia from trading in its debt on US and European markets along with similar sanctions on members of the lower house of the Russian parliament who voted in favor of the recognition of the breakaway regions. The US has also committed to sanctions against NordStream2 AG (parent company of the NordStream2 project).

UK Sanctions (Pre Invasion)

UK sanctions included sanctions against Rossiya Bank, IS Bank, General Bank, Promsvyazbank and Black Sea Bank. The UK will also join the EU and US by prohibiting sovereign debt issuance in the UK. The UK is also sanctioning 3 Russian billionaires that hold positions in the oil & gas industry and finance industry.

german sanctions (pre Invasion)

Even though Germany is a Core EU nation, German “sanctions” came in an unorthodox fashion. In addition to the umbrella of EU sanctions, German Chancellor Olaf Scholz announced the halting of plans to execute Gazprom’s (Russian oil firm) $11.6 billion project “NordStream2”. The project was intended as a 1,230 kilometer pipeline that would supply 151 million cubic meters of natural gas per day.

Japan Sanctions (pre Invasion)

Japan’s sanctions included banning issuance of Russian bonds in Japan as well as restricting travel to Japan for select Russian individuals.

Invasion Launch

It is ever so evident that despite the aggressive and highly-concerned undertones expressed in the UN Security Council meeting on 02/21/2022, the sanctions imposed against Russia have been relatively light in contrast, but now that we have now endured what many global leaders feared would happen… a Russian invasion of Ukraine, we have seen an additional layer of sanctions added to the Russian economy.

EU Sanction Playbook

Extended EU sanctions against Russia will increase the number of Russian banks blocked from EU financing. Bank Otkritie, Alfa-Bank, and various lending organizations have been added to the financial blacklist for the EU in addition to the pre-invasion sanctions as-well as Russians being limited to depositing no more than 100,000 euros in EU banks.

Russian aerospace and defense companies were also sanctioned by the EU with securities transaction and lending restrictions imposed on the heavily state-owned sector. Export limitations on goods that serve as benefit to the Russian military such as, but not limited to, sensors, telecommunication hardware, and lasers have been imposed as-well.

US Sanction Playbook

The US has imposed very meticulous financial sanctions on Russian financial institutions. As per the US Treasury, “Treasury is taking unprecedented action against Russia’s two largest financial institutions, Public Joint Stock Company Sberbank of Russia (Sberbank)and VTB Bank Public Joint Stock Company (VTB Bank), drastically altering their fundamental ability to operate. On a daily basis, Russian financial institutions conduct about $46 billion worth of foreign exchange transactions globally, 80 percent of which are in U.S. dollars. The vast majority of those transactions will now be disrupted. By cutting off Russia’s two largest banks — which combined make up more than half of the total banking system in Russia by asset value — from processing payments through the U.S. financial system. The Russian financial institutions subject to today’s action can no longer benefit from the remarkable reach, efficiency, and security of the U.S. financial system. The US Treasury also disclosed sanctions, “on three additional major Russian financial institutions: Otkritie, Novikom, and Sovcom. These three financial institutions play significant roles in the Russian economy, holding combined assets worth $80 billion. These designations further restrict the Russian financial services sector and greatly diminish the ability of other critical Russian economic sectors from accessing global markets, attracting investment, and utilizing the U.S. dollar.”

The US has also decided to pursue sanctions against Russian individuals.

Japanese Sanction Playbook

Japan has also targeted Russia’s financial sector by imposing sanctions on Promsvyazbank, Bank Rossiya and Russia’s economic development bank VEB.

Japan has also avoided targeting Russia’s energy exports in their second set of sanctions.

Overview of Imposed sanctions

There has also been more participants such as South Korea, and the UK who have imposed sanctions on Russia; carrying parallels to the US, EU, and Japan. Global sanctions on Russia’s energy exports have been absent.

Collateral Damage

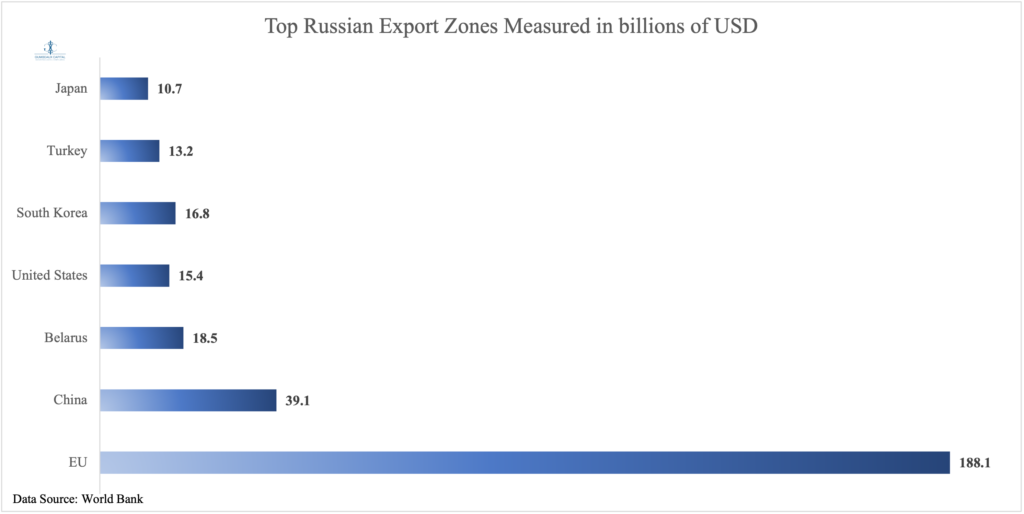

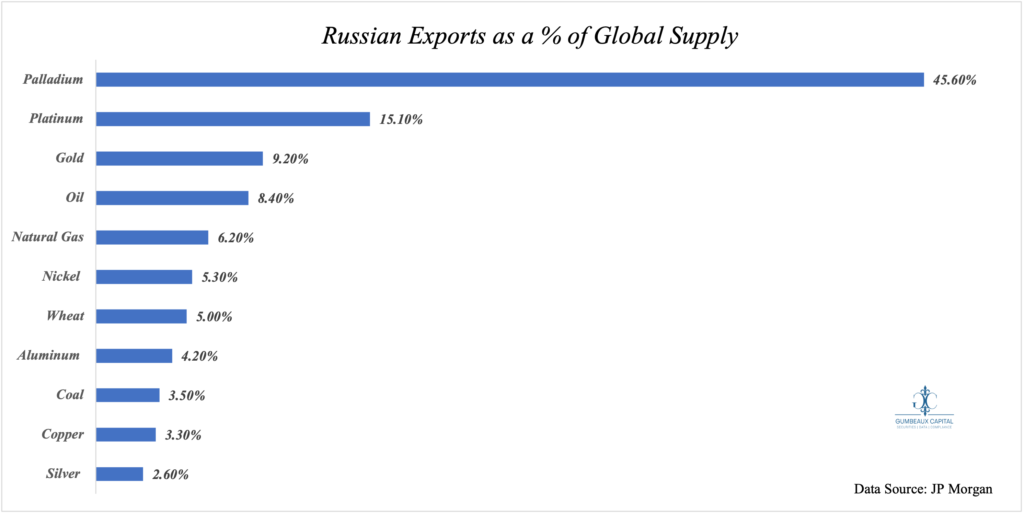

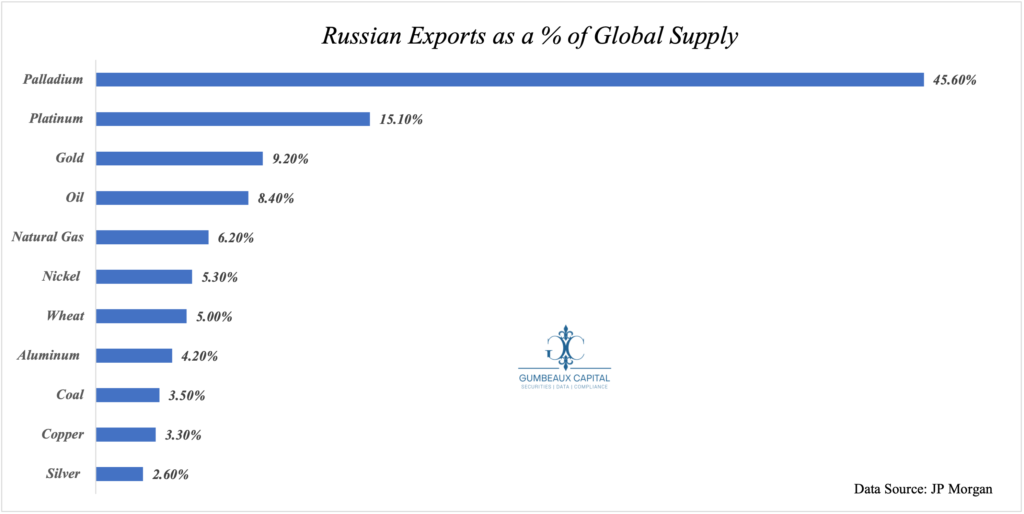

A large question at hand following the sanctions that have been imposed on Russia’s economy is if the economic risk will be felt not only in Russia, but if the effects will felt by its economic partners and adversaries? First we must take a look [Figure 2] at who Russia’s largest trading partners are and what Russia exports to the world in abundance amidst a global goods supply “struggle” [Figure 3]:

EU Dynamics

The EU has been dealing with a debilitating energy crisis preceding the Russian invasion of Ukraine, and given that the largest composition of goods imported from Russia fall under the energy basket (at 63% of all EU imports from Russia as of 2020), we can note that this was a catalyst of leaving out energy sanctions. This was extrapolated as Brent Crude exceeded $100 on the fears of sanctions against Russian energy exports.

The financial sanctions imposed against Russia from the EU in tandem with the US has led to the 45% decline in the MOEX index, and Russian 5-year credit default swap spiking approximately 178% from the start of 2022.

Chinese Dynamics

It is well known that China and Russia carry a close, but uncanny relationship with China. The Russia-China relationship has undoubtedly grown closer due to what both countries see as a relationship of “convenience” to strategically counter the feeling of a western-derived “existential threat” against their existing authoritarian regimes; in particular, the US’ “hegemonic power”

Bounded in particular by the notion that Moscow understands it cannot resist the US’ hostile economic and political stance against it without the economic leverage from Beijing; correspondingly Beijing understands that Russia provides value in its relative advantage in military technology. As quoted from the OSW’s Beijing-Moscow Axis, “This is the area of greatest differences between the partners, in which they can even openly compete with each other as they pursue their own individual interests. However, this happens largely without damaging the integrity of their relations. Central Asia occupies a special place in their relationship, since it is the immediate strategic hinterland for both. Therefore, even though the region is the object of their competition, they coordinate their actions here to a greater extent than anywhere else (see Part V). Chinese experts believe that the Russian Federation only pursues an active policy in those parts of the world where it can use its only asset i.e. military power. Since Beijing prefers a strategy based on economic expansion, the partners can pursue complementary activities, as was the case with the 2019 crisis in Venezuela. In some cases, Russian security involvement is concurrent with the PRC’s economic interests, as in the Central African Republic: although from the point of view of the CCP elite, the line between Moscow offering its ‘security services’ in the Third World and deliberately creating a demand for it is blurred.”

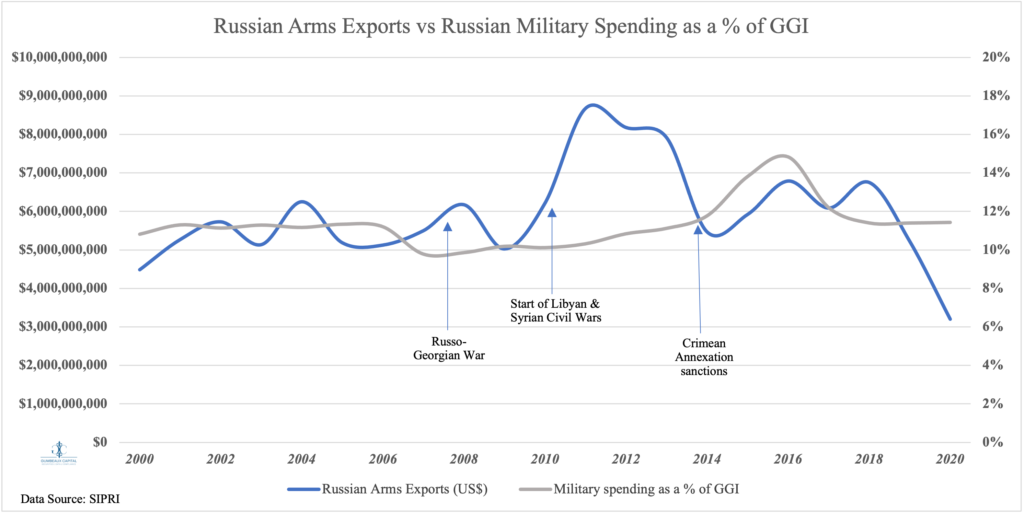

Provided the pretext on Russia’s military based advantage, we should take a look at the true value in its economic context: As SIPRI reported,” Russian arms exports in 2016–20 were at a similar level to 2001–2005 and 2006–10 but were 22 per cent lower than in 2011–15, when Russian arms exports peaked. While Russian arms exports in 2016–18 remained at a relatively high level, they fell in both 2019 and 2020. The overall decrease in Russia’s arms exports between 2011–15 and 2016–20 was almost entirely attributable to a 53 per cent drop in its arms exports to India. This decrease was not offset by large increases in Russia’s arms exports to China (49 per cent),” we can note that China has become a “baseline buyer” [as expected] for the Russian arms exports. This has kept Russian defense companies active despite Russian defense military spending as a % of GGI stabilizing (with some [Crimean Annexation + Sanctions] exceptions) between 10-12% (See Figure 4).

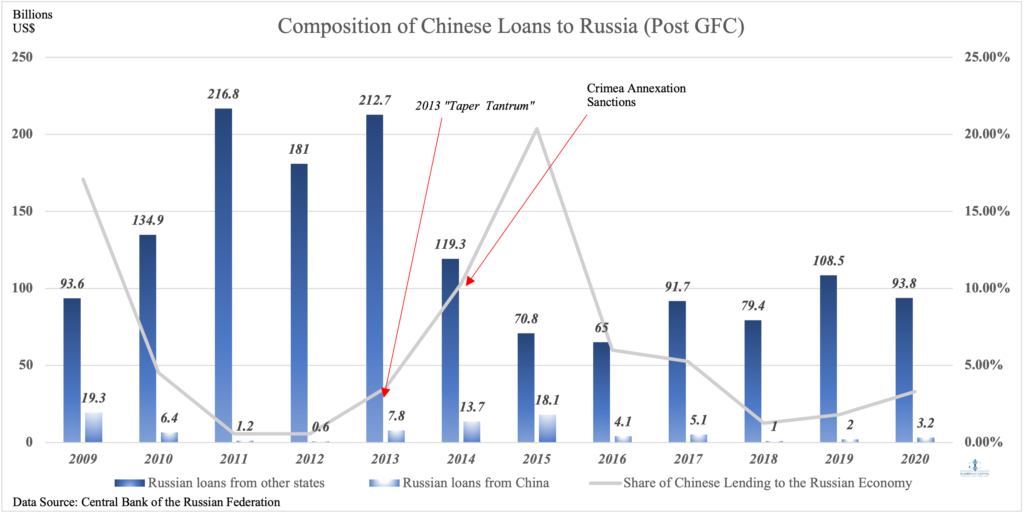

China has also, reluctantly, been a pseudo-strong supporter to the Russian financial sector. As per the OSW Beijing-Moscow Axis Report,”Financial cooperation, including Chinese loans and direct investments in Russia, is generally limited and confined to selected sectors of the economy. The way Chinese capital is utilised deepens the model of centre‐periphery relations, where raw materials from the Russian Federation are exchanged for industrial goods from the PRC. Money flows predominantly towards strategic energy and mining projects carried out by policy banks and state‐owned companies. A more ‘organic’ and commercially‐led inflow of Chinese capital from commercial banks and private investors – a potential alternative to Western funding – has encountered significant barriers: Beijing’s fear of being targeted by Western sanctions, an unfriendly business environment in Russia, and also its reluctance to sell key assets. As a result, Chinese money still has not filled the visible gap left by EU and US investors and lenders in the Russian Federation since 2014.” These dynamics are heavily extrapolated [Figure 5] as it is evident that Chinese liquidity is heavily utilized in risk events affecting Russia’s financial system in terms of inflows. Taking this dynamic into account, we can certainly expect China to do the same for Russia following the most recent western sanctions.

Albeit China serving as the liquidity “haven” for Russian risk-on events, China is still facing their own liquidity issues that could pose as detrimental over time to the existing mechanisms put in place to mitigate risk for their psuedo-ally. This overlying sentiment of risk has also bolstered the exorbitant jump in Russia’s 5-year CDS.

Belarusian Dynamics

Facing the brunt of collateral sanctions for expressing support of Russia’s invasion of Ukraine, Belarus will likely remain unfazed at the macro-level following the Russian sanctions. Unsurprisingly, Russia’s main export to Belarus is energy products and equipment which has avoided sanctions from the west. The main effect regarding this bilateral trade partnership will be financial liquidity shortages due to banking sanctions from the west.

US Dynamics

The US has taken a very similar approach to the EU with sanctions against Russia by limiting their risk against the structural oil & gas supply constraints via avoiding sanctions against Russia’s energy and petroleum exports. The US has also contributed to the impending financial liquidity crisis in Russia [Russian 5-yr CDS]. It is also key to note that the US is significantly less reliant on Russia for its oil and gas supply relative to the EU, and has many supply-side hedges against the political risks associated with the current environment within US-Russian relations; such as, but not limited to, SPR releases.

What does this mean for russia?

While it is ever so tempting for many to speculate politically, we will leave that up to the policymakers, but economically and financially Russia will see very limited effects of sanctions and its own invasion in the short-term as their energy exports and natural resources still provide ample economic value to the world, and inherently its domestic economy [See Figure 6].

It is also key to note that if Russia is successful in their efforts to encompass Ukraine for economic leverage, Russia may have sovereign control of the resource rich Ukraine containing an ample supply of goods such as, but not limited to: Barley, Wheat, Corn, Natural Gas, Coal, Lithium, and increased strategic access to the Sea of Azov.

The marginal benefit for Russia may be dwindling due to hyper-complex political dynamics, and investor sentiment has reflected so as the mentioned move in Russian 5-Year CDS’ and the all-time low move in the Russian Ruble in FX markets.

Wrap-Up

As any military conflict would carry volatility, the Russian invasion of Ukraine has certainly created a perfect storm for volatility. Equity markets will likely extrapolate and perpetuate the dynamics we expressed in our 2022 macro outlook. FX markets will experience increased volatility due to effects of forward expectations in interest rate parity; in particular, the notion that the Russian invasion may perpetuate the European energy crisis, and may deter the ECB from their impending normalization policy. We should also expect further easing in the Chinese economy as they will likely set up liquidity-providing mechanisms for Russia as-well as their own domestic needs. This will increase the risk sentiment surrounding Emerging market growth as these events will certainly continue to make the global aggregate growth picture slightly dimmer. In due time, “safe havens” will be the dominant force in financial markets.

In the longer term perspective, keying on assets that serve as substructures of more-efficient supply chains (i.e., logistics, transportation, procurement etc.) will be critical. Energy equities with high 2021-early 2022 CapEx [as we briefly mentioned here], and or, strong and consistent free cash flow starting Q2 2021 will serve as great opportunities to capitalize off the existing and potentially lingering dynamics within the global energy sector.