As 2021 comes to an end, we are left with many reflective dynamics in regard to the global economy and the financial markets. From growth-optimism, reflation, inflation, and now liquidity variance, 2021 has set us up with an extremely pivotal 2022.

Pivotal Policy

The global monetary policy environment will be a key focus in 2022, as various leading economies seek policy shifts, and some seek policy perpetuation. This dynamic has brought upon some polarization in the global aggregate policy stance; particularly the contrast between emerging markets and top developed markets.

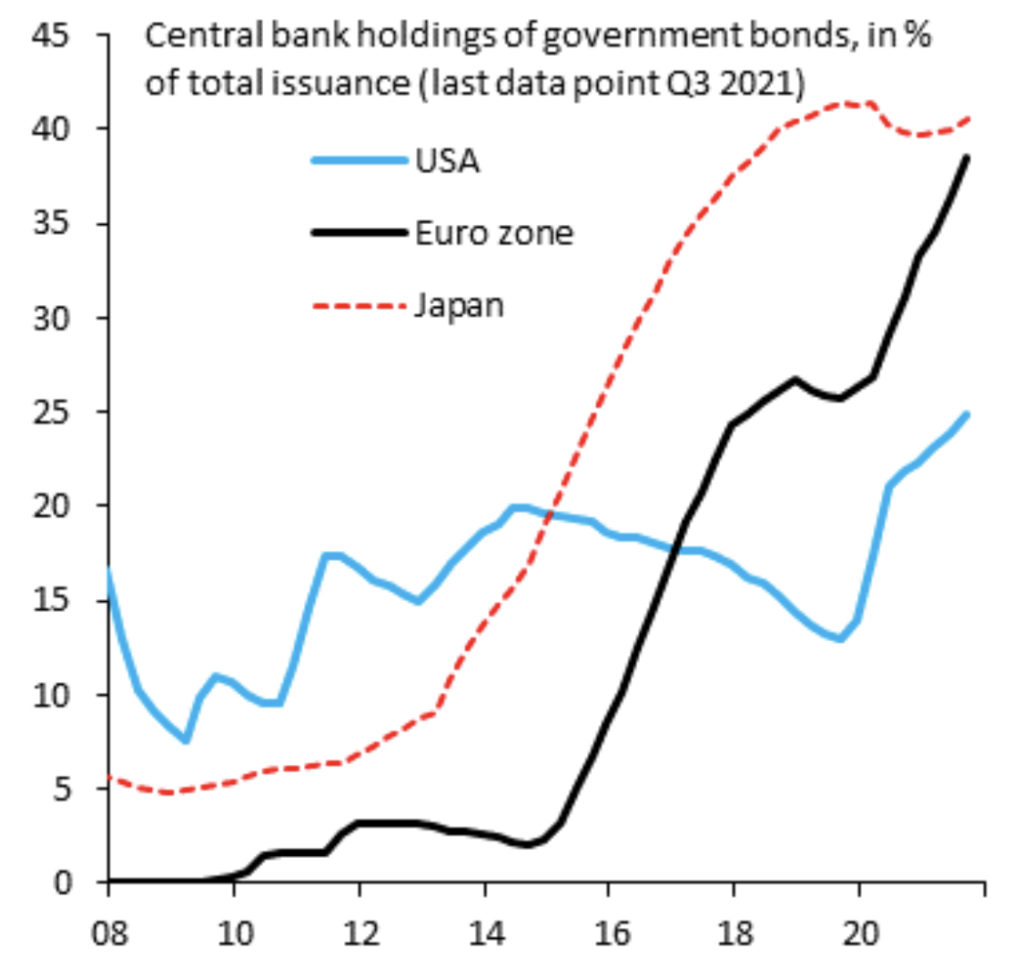

Given that liquidity has been the driving force for markets throughout the entire previous cycle, it cannot be disregarded when contextualizing the dynamics of the upcoming economic cycle. To properly contextualize what will be evident in the upcoming economic cycle, we must assess the largest players in global liquidity and their liquidity instruments.

With all 4 of the leading economies implementing accommodative policies throughout the pandemic and 1H 2021, it has caused an interesting picture in terms of real rates. Given that “unconventional” monetary policy was the dominant force in nominal rates over this cycle of accommodative policies, the forward capacity of debt capital markets and money markets have served as the leading principal on capital flows. This is why policy has now become very pivotal in the recovery phase for the developed economies, as capital flows and investment will be the key driver of long-term growth in lieu of government expenditures (the key driver of the 2010s), and net-exports (de-globalization thematic).

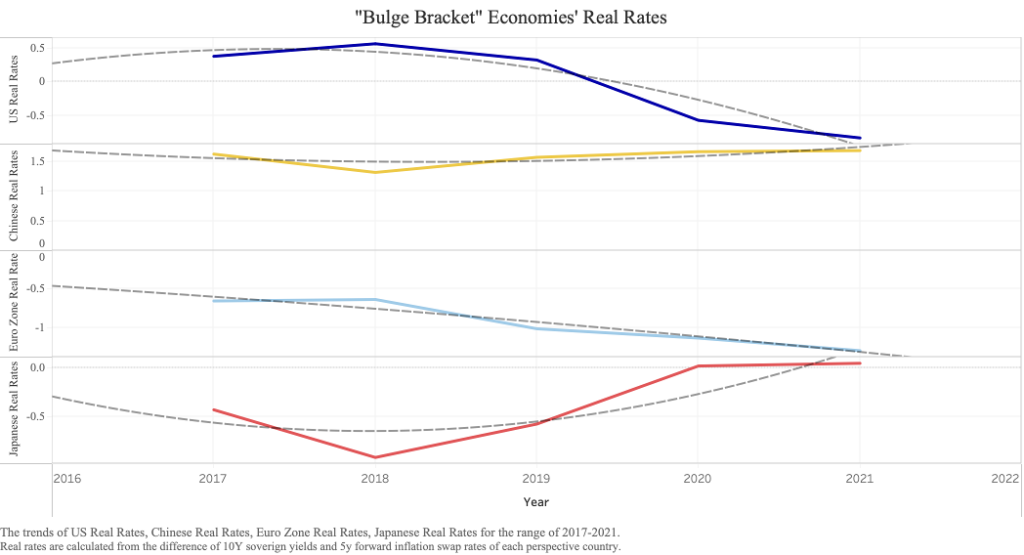

To unpack this, when looking at the developed basket’s real rates (Figure 1), we can see that all of the top 4 economies are ranging close to the 0% mark, and in the case of the US and the Euro-Zone, we can see negative real rates. With China and Japan, we can see real rates remaining rangebound right above the 0% mark. The real question is, will these trends perpetuate?

US Real Rates

For the United States, the picture is likely the clearest. With an expected hawkish stance from the FOMC minutes on Wednesday, January 6th, 2022, we will continue to see a tapering in asset purchases from the Fed and nominal rate hikes until the Fed can reach their price stability mandate.

There are still some risks to the tapering and tightening picture though. For example, the Fed still has a close eye on employment figures, and more closely on the labor-force participation rate (LFPR) in particular. With a record number of 4.5 million people leaving their jobs in November, and relatively robust JOLTS reports, these conditions may create some turbulence in the steadfast tapering framework from the Fed. This may lean the Fed to keep credit spreads relatively tighter to accommodate the labor force respectively for the time being before their first FOMC meeting in late January, and or the following FOMC meeting in mid-March. Nonetheless, short term securities will certainly experience high volatility until the Fed decides on a set benchmark for nominal rates.

Although, to no surprise, the Fed will look to increase rates to curb recent inflationary pressures within the US economy. Inflation was the key driver of sending real US rates into negative territory, but how much can the Fed do to curb inflation?

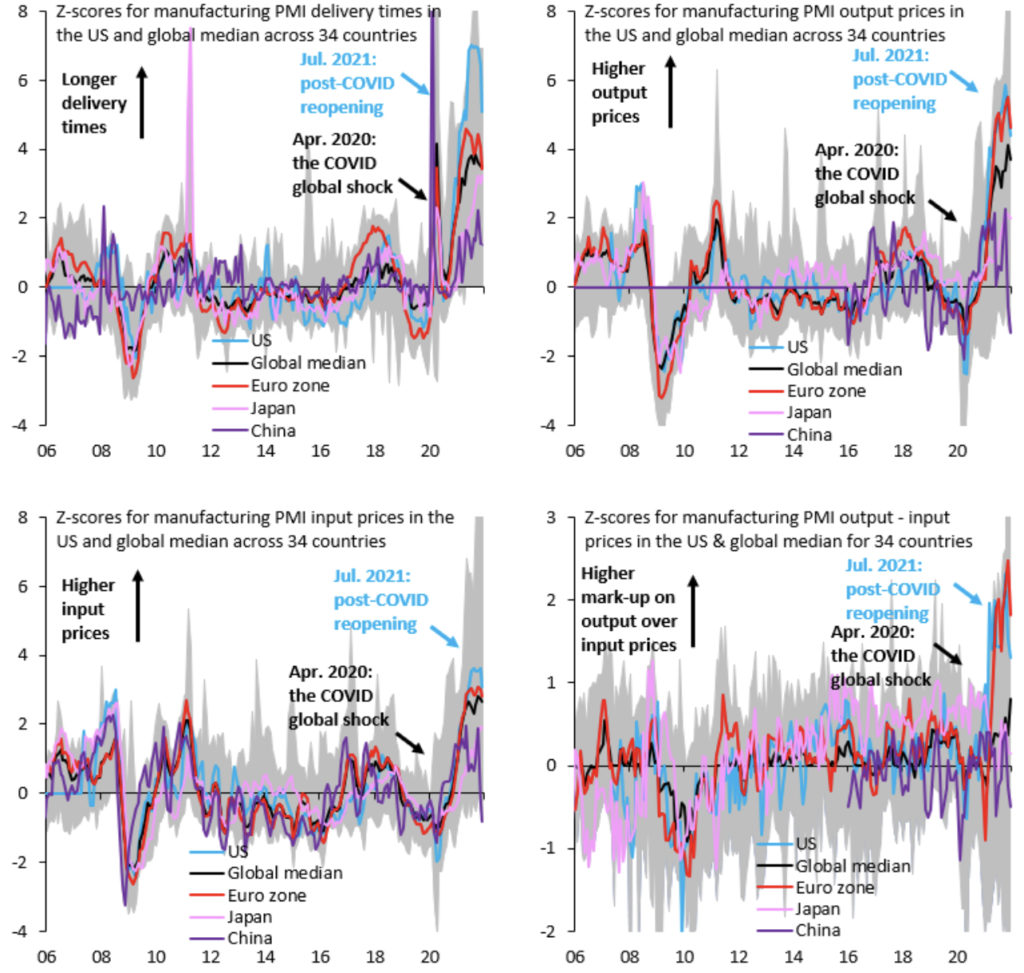

As we can see in Figure 2, the thematic of the supply chain crisis is now waning, and long-run aggregate supply isn’t as much as a worry (ceterus paribus) as beforehand, but with tighter financial conditions comes tighter growth conditions, so unless there is another serious demand shock… (which despite the US having its highest Inflation prints since 1982, US consumer confidence ended 2021 on a high note) short-run aggregate supply may be at detriment. This could cause the economy to undershoot its supply equilibrium, and keep price levels higher than intended thus elevating the 5y/5y forward swap rates, and subsequently lowering real rates (regardless of where 10y-yields head towards). In the event that this happens, long-run aggregate supply will be at risk again, and so will employment figures (natural rate of employment = LRAS) leaving financial and economic conditions where they remain today.

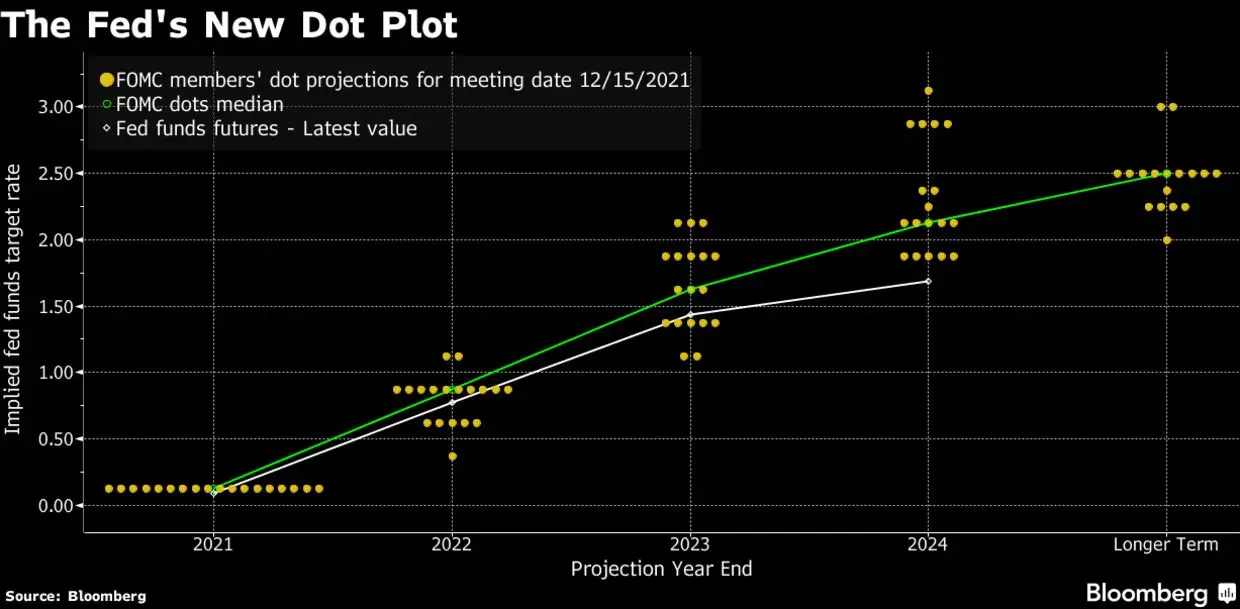

Given that long term growth is going to be dependent on inflows to capital markets to service the debt of today’s (growth-oriented) expenditures, the Fed may undershoot the general hawkish expectations (Figure 3), and take more of a steady (still hawkish) approach to their tightening framework relative to the recent aggressively hawkish tones from Fed affiliates, in aim to promote risk-stability in markets while easing inflationary pressures.

Chinese Real Rates

The Chinese picture is an interesting picture, as China has now implemented itself into the “bulge bracket” economies, and is the core of the global supply chain for a large basket of goods. China is likely at the most pivotal point regarding policy from an internal standpoint, as they aim to solidify themselves as an economic powerhouse and shift the global economy to a multipolar setting regarding the US.

Nonetheless, China has some complex idiosyncratic risks. Luckily for China, they have positive real rates to work with, which indicate that they have a bit more room to proceed with more accommodative economic policies before capital allocation indifferences become a risk on forward growth (rising real rates from global counterparts).

With the general economy pointing China at lower growth targets for 2022 (sluggish retail sales, and the real estate liquidity crisis), the PBOC may look to keeping the premium of higher real rates via tightening credit conditions, but accommodating for liquidity needs via unconventional policy. To further contextualize the Chinese picture… as the US looks to taper and tighten, the Chinese may look to only taper as they have the suitable capacity to do so. This is further reflected as PBOC Governor Yi Gang recently “vowed to keep a “normal” monetary policy for as long as possible and avoid large-scale stimulus.”

All in all, as long as the risks from the leverage busts in the Chinese real estate sector, remain akin to the sector and akin to the local economy, and or can possibly be mitigated… look for Chinese growth to continue on a healthy trend, unless there is another serious global and domestic demand shock.

Euro-Zone Real Rates

In the Euro-Zone’s environment, things prove to be pretty tricky as the decline real rates begins to steepen (50bps since 2017). Given that Euro Zone 5y5y forward swap rates remain steady, and even slightly decreasing, we can attribute the fall in real rates towards the aggressive ECB QE (Figure 4).

Even though the “ECB Governing Council judges that the progress on economic recovery and towards its medium-term inflation target permits a step-by-step reduction in the pace of its asset purchases over the coming quarters,” the ECB still remains widely accommodative relative to its “bulge bracket” counterparts. The ECB suggests that, “monetary accommodation is still needed for inflation to stabilise at the 2% inflation target over the medium term. In view of the current uncertainty, the Governing Council needs to maintain flexibility and optionality in the conduct of monetary policy,” thus the “Governing Council decided on a monthly net purchase pace of €40 billion in the second quarter and €30 billion in the third quarter under the APP. From October 2022 onwards, the Governing Council will maintain net asset purchases under the APP at a monthly pace of €20 billion for as long as necessary to reinforce the accommodative impact of its policy rates. The Governing Council expects net purchases to end shortly before it starts raising the key ECB interest rates.”

Pairing this dynamic with the fact that Italy and Germany are sitting at the top end of global unemployment rates, we can conclude that the Euro Zone has a LRAS, and aggregate demand issue. This indicates that the optimal policy stance is out of the hands of the ECB at this point, and a collective fiscal effort of the ECB is greatly needed to protect long term growth objectives, and to hedge against any impulses in growth for the near-term.

Euro Zone Governments may be reluctant to provide ample fiscal support to the economy as the Euro remains relatively strong, as even with an extremely strong USD, the EUR/USD spot continues to trade at 1.13 which makes it certainly hard for the Euro Zone to reflate to optimal price levels in real terms. This in turn, may lead to a rate target stagnation from the ECB which can possibly ease Euro strength, induce aggregate demand, and allow EU nations to actively assess their perspective fiscal environments to support LRAS (+ natural rate of employment.)

Japanese Real Rates

With Japan sitting at positive real rates for the first time since initial QE, there are a some dynamics to question. Given that 10y yields have remained relatively unchanged since 2017, but real rates have risen accordingly, we can attribute this environment to the lingering “under-inflation” that Japan deals with. Despite energy and food costs are pushing up prices in Japan, inflation remains well below the BOJ’s 2% target as weak consumption discourages firms from passing on higher costs to households. A BOJ member even stated, “Monetary policy will be normalised in Japan when the price target is achieved in a stable manner irrespective of policy developments in other economies,” “Given the target has not been achieved, there is absolutely no reason to adjust monetary easing.”

Japan’s situation is highly similar to the EU, but with a relatively weaker currency, and a deeper structural “under-inflation” issue. Further accommodative policies are inevitable in Japan, and the Yen should counterintuitively stabilize if the BOJ can meet its targets due to the fact that the “under-inflaton” is derived from a lack of aggregate demand.

Consumer confidence, lending activity, and net exports will be the key indicators on the future dynamics of the Japanese economy, and its safe haven status.

Risk Dilemma

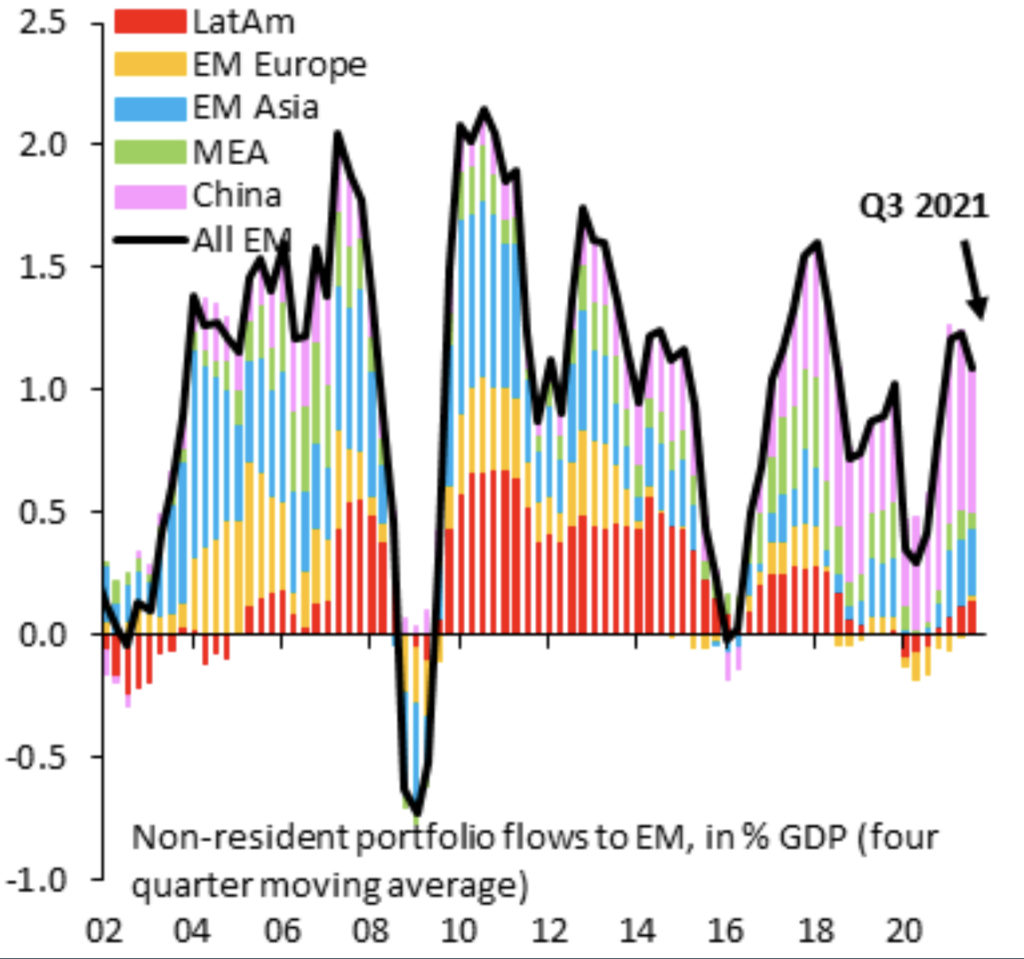

Given that our “bulge bracket” of economies are dealing with some robust uncertainties going forward, the search for a “safe haven” may be tricky… This can be extrapolated with the EM capital flow environment (Figure 5).

This shows that EM portfolio flows outside of China have been non-existent, signaling an illiquidity crisis going forward for emerging markets excluding China. Despite emerging markets offering higher relative yields than “bulge bracket” safe haven nations, tighter aggregate financial conditions may reduce the already drying up liquidity from the EM basket. 2022 will certainly not be the best year for EMs as a whole (Debt, Equities,FX).

FX

Carrying on from the EM risk dilemma, the FX outlook is simple “bulge bracket” (USD, EUR, JPY, CNY) vs EM, and given the idiosyncratic position of the US… look for USD to continue dominate the FX markets in 2022 from a liquidity standpoint, and a fundamental standpoint.

Equity Fallout

The same dynamic we see in the aggregate market for EM’s is the same dynamic we will see for equities. An aggregate tightening in credit conditions, and a subsequent tightening in monetary policy will reduce aggregate liquidity from the equity markets as per expected, but given that the entire previous cycle was derived by accommodative policy and looser credit conditions, liquidity dynamics have allowed equity valuations to rise above fair and earnings based equilibriums.

Given, equity prices are currently subject to the forward ability for companies to generate increased free cash flow and earnings, but with a net tightening on financial conditions, we just do not see how aggregate demand will sustain itself to continue to boost FCF and EPS; allowing for an imbalance fill in equity indexes and individual equities respectively.

Digital Assets

Just as we covered with equities, digital assets will see price levels return to their intrinsic valuations with respects to their aggregate demand. The liquidity driven market may be primed to be hit the hardest in the midst of tightening financial conditions.

Commodities

Within the area of commodities, in 2022, energy will take the spotlight. As energy production and provision travels through regulatory headwinds, there are plenty of fundamental/demand derived tailwinds for the energy sector.

Nonetheless, inventory dynamics (build/draw) will be the core price determinants, and liquidity buffering will subside for the FY2022.

Oil

Oil prices may stagnate due to the fact that oil demand will continue to catch up to the current price equilibrium, but will be mitigated by non-OPEC producers servicing the market in ample volumes.

It is also key to note that open interest on oil has hit a cycle low even with a spot price above $70/bbl.

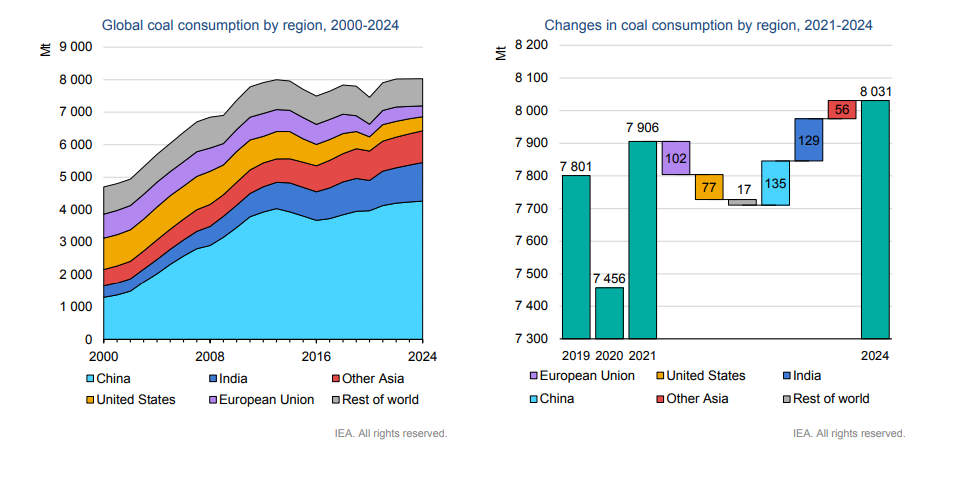

Coal

With many regulatory headwinds locked on to coal, coal prices will certainly experience some volatility. One thing to keep an eye on will be the dynamic that coal demand is poised to increase throughout the next 3 years (Figure 6)

Precious Metals

Precious metals will face headwinds from net policy shifts, and subsequently changing liquidity dynamics. Albeit the inflation cloud still looms over the global economy, precious metal prices should see short term volatility until there is further net-clarification on the global policy stance.

Industrial Metals

Aluminum and copper will be the focus of the industrial metal sector where both metals face supply side volatility due to regulatory headwinds.

Aluminum

Aluminum production will continue to further be constrained by the net-0 policies across the globe to to the high carbon output aluminum production carries. This dynamic could certainly create an upside imbalance for aluminum as demand will inelastically rise despite the supply-side headwinds.

Copper

As many large miners scale back their copper extraction, copper inventories are poised to overshoot equilibrium value to maintain price, and with a stronger dollar In the picture, copper prices may experience downside pressures in 2022.

Agriculture

Global agriculture stocks (inventory) have been persistently lower throughout 2021. Dependent on the increasingly volatile weather dynamics (La Niña), the outlook on agriculture stocks (inventory) are unclear at the moment. Nonetheless with supply chain bottlenecks looking to ease, agriculture goods prices should slightly lower in 2022.

Fundamentals (Cycles) Matter!

2022 will not be a simple market to participate in relative to the past 3 years. Liquidity will be reduced as we enter a net tightening of financial conditions, and fundamentals will reign as king again. Growth (LRAS) and aggregate demand will be the key determinants of liquidity (inflows), and defensives should be a top priority for each investor’s portfolio for 2022.