It has been nothing short of a war between economists over if we will see out hyperinflation or deflation in result to the COVID-19 economic recession, and the aggressive monetary policy enforced by the Federal Reserve. Many argue that the quantitative easing, or “QE” performed by the Fed will ramp up monetary supply, and subsequently conjure hyperinflation.

Limitations to QE

First, we must look at what the renown Fed “QE” is. The root of the Fed’s “QE” is the multitude of repurchase agreements, or better known as a “repo”. What is a “repo” you might ask? A repo or repurchase agreement is used to raise short-term capital through short-term borrowing for a dealer. In this case the Fed is the dealer. The Fed sells government securities in the form of treasuries to investors overnight and will repurchase them the next day at a higher price at the overnight interest rate. The buyer plays as a short-term lender and the seller plays as a short-term buyer to stimulate the liquidity and funding targets. This is a tool that the Federal Reserve use to increase the monetary base within the economy. This paired with a rise in the Fed’s increase in its balance sheet holdings, ULRIP (Ultra-Low Interest Rate Policy), and fiscal stimulus administered by the treasury, has led to an increase in the monetary base and money stock, but not the highly misconceived direct increase of monetary velocity.

Contrary to misconceived belief, money supply can only increase if banks lend to businesses and consumers. QE initially increases the amount of bank deposits those companies hold (in place of the assets they sell). These companies will now look to balance their portfolios of assets by buying “high” yielding assets and inflating the price of those assets and stimulating spending in the economy. Therefore, you have seen bearish imbalances, post COVID selloff, become filled within high yield assets, like equities/stocks, and a very suppressed bond yield. In result of QE, new central bank reserves are created. But once again these are not a catalyst of monetary velocity.

Inflationary Refutation Imminent ?

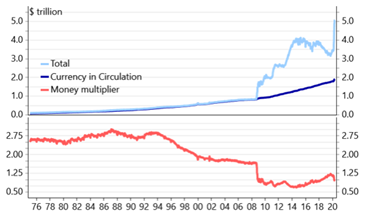

Whilst money supply has risen substantially, there has been an extreme divergence within monetary supply and the monetary multiplier (see chart1), which is a measurement of the “effectiveness” of monetary policy. While yes, there has been a substantial increase of money supply, which is very traditional in deflationary recessions in reach to create an economic “equilibrium”. This has been the catalyst for the recent recovery in CPI and core inflation. So yes, the short-term inflation will be alive and well, but far from sustainable.

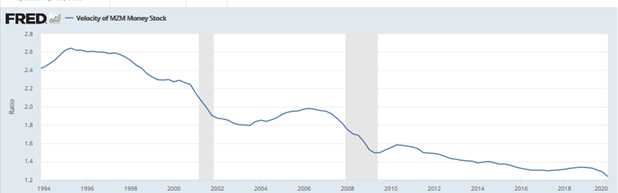

Long-term inflation risks have been counter-complimented by a sharp decline in monetary velocity, which is a measurement of the rate at which money is exchanged in an economy (see chart 2). This creates a tough environment for inflation to reach ample targets, let alone the likelihood of any form of hyperinflation.

Going Forward

While yes, we may experience equilibrium-oriented inflation in Q3 2020, as we have uncovered, this trend is highly unlikely to remain sustainable; along with the suppression of bond yields. Look for credit risks to continue to rise, and a deflationary setting within risk assets, and goods heading into Q4 2020. This should be followed by a further tightening access to credit, and an increase in the likes of mortgage rates. Market forces do not always lead individual banks to sufficiently protect themselves against liquidity and credit risks. Because of this, federal regulations aim to ensure that banks do not take excessive risks when making new loans, including via requirements for banks’ capital and liquidity positions. These requirements can therefore act as a resistance on how much money commercial banks create by lending. Look for “Safe-haven” assets to recapture lost liquidity moving into Q4 2020 and in H1 2021.